Every mortgage lender provides their unique DTI constraints

Summation? The best DTI is 0%. Very try not to attract so much in your matter-work with repaying your debt.

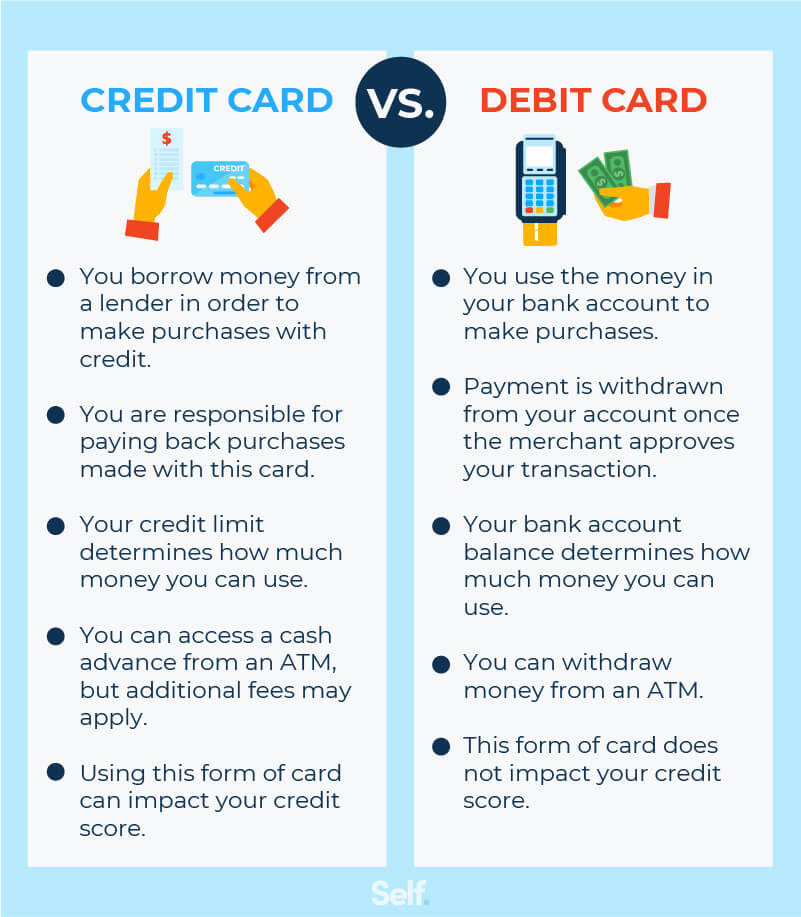

Debt-to-Income Proportion to possess Mortgage loans

Whenever making an application for a home loan, loan providers will look on a couple different varieties of DTI rates: a front side-prevent proportion and you may an ago-end proportion.

Front-avoid ratio: A top-stop ratio merely is sold with your own complete month-to-month houses will cost you-such as your lease, homeloan payment, monthly property owners association fees, possessions fees and you will homeowners insurance.

Lenders like your maximum front side-prevent ratio is twenty eight% or down. However, we recommend you keep your own overall houses will set you back to zero over twenty five% of get-household pay to end becoming what is called home bad.

Back-end proportion: An in the past-prevent ratio (that is what the DTI Proportion Calculator over provides you with) comes with your own monthly houses will set you back along with various other month-to-month obligations payments you may have, including credit cards, student education loans otherwise medical expense. Lenders generally speaking care much more about the rear-prevent proportion because provides them with a far greater picture of your average monthly installments.

Such, the Government Construction Government (FHA) allows you to have a top-prevent proportion of 31% and a before-stop proportion off 43% to be eligible for a keen FHA loan. 1

How to Lower your Personal debt-to-Earnings Proportion

If for example the blood pressure raised when you watched their DTI, take a deep breath. You do have more control more one to amount than you possibly might consider!

The answer to cutting your DTI will be to reduce your month-to-month debt otherwise increase your monthly money. Or even better, both! Here is what you could do to lessen your debt-to-earnings ratio.

Do not accept anymore obligations.

The company-brand new vehicles that is calling the identity? You to vessel you have been eyeing for a long time? You’re only financing or a few of leading them to yours. Nope, hold on loans Waldo a minute right there! Credit more income will just build your DTI payment increase (and have stress peak). You may be inclined to add more costs toward dish, but you should really be working to eliminate the repayments you have.

Improve earnings.

Get a few extra instances at your workplace. Snag a side hustle. Inquire about a boost. Everything you will perform for lots more currency to arrive each few days can assist reduce your DTI. But don’t just earn more income in the interests of boosting the debt-to-money proportion. Fool around with you to definitely more money to settle the debt too!

Minimal costs equivalent restricted improvements. Surely, when you’re simply expenses the lowest repayments in your bills for each and every week, those people balance usually loaf around forever. And you will nobody wants one. To settle financial obligation faster, start with tackling their tiniest financial obligation basic-maybe not the main one into the high interest rate (we phone call which the debt snowball method). If you are using the debt snowball means, you are getting quick wins and discover advances instantly. And you will that can motivate you to pay off the rest of your obligations even faster.

Log in to a resources.

Getting a cost management app (such as for instance EveryDollar) wouldn’t help make your DTI proportion amazingly shrink. Exactly what a resources is going to do is make it easier to aesthetically select in which your finances is certian every month and you can tune where you stand overspending. For many who cut back in those portion, you’ll have additional money to help you put at the financial obligation every month-that will decrease your DTI (and get your nearer to a lives rather than obligations carrying you back).

The truth about Financial obligation-to-Income Ratio

Many companies would say one to maintaining your obligations in the an amount you could would try an indication of a good economic health. However, let’s not pretend. Even in the event your own DTI proportion is regarded as a great, one to nonetheless mode more a 3rd of paycheck is going so you can things you never very own. Yes, it will be manageable because of the a beneficial lender’s criteria, but can you wanted anywhere near this much of your own income supposed into the another person’s wallet?

No Comment